Irs Annuity Tables

What Do The New Irs Life Expectancy Tables Mean To You In 2021 Retirement Financial Planning Irs Life Expectancy

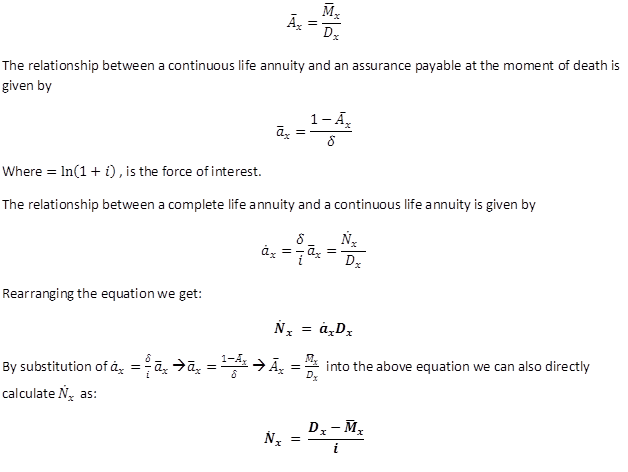

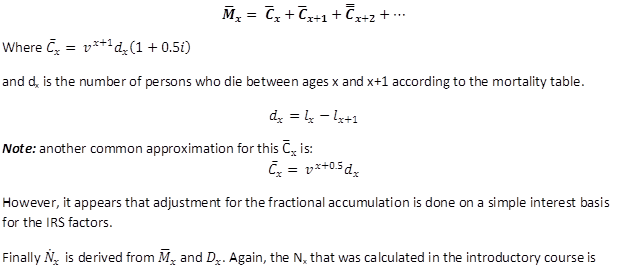

42 4 2708 Determining Present Value For The Endowment Credit Administrative Rules Of The State Of Montana

Irs Issues Applicable Federal Rates Afr For September 2020

Irs Tool Estimates If You Will Get A Tax Refund Or Owe Money Tax Debt Tax Deductions Tax Guide

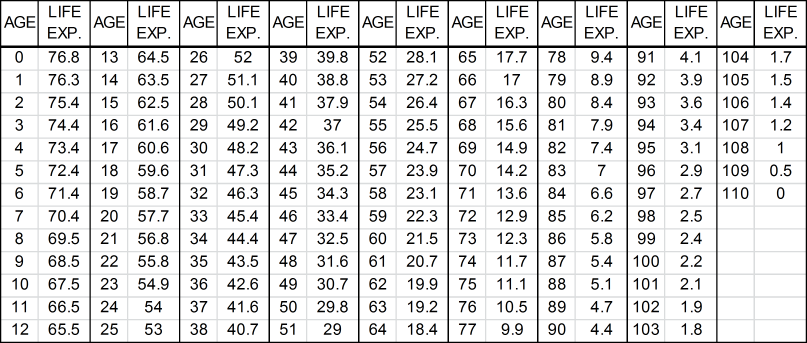

Life Expectancy Tables Actuarial Life Tables

Required Minimum Distributions Required Minimum Distribution Retirement Calculator Life Insurance Quotes

Table I Single Life Expectancy For Use by Beneficiaries Age.

Irs annuity tables. The tables below contain the historic rates of the month starting in January 1989. These regulations affect participants beneficiaries and plan. Mortality Improvement Rates and Static Mortality Tables for Defined Benefit Pension Plans for 2022 published in IRS Notice 2020-85 on December 14 2021.

3158 Investment in the contract adjusted for value of refund feature. 18 Percentage from Actuarial Table VII for age 65 with 18 years of guaranteed payments. These actuarial tables do not apply to valuations under Chapter 1 Subchapter D.

Thus retaining the mortality tables. The life expectancy and distribution period tables that are used to calculate required minimum distributions from qualified retirement plans individual retirement accounts and annuities and certain other tax-favored employer-provided retirement arrangements. The life expectancy tables and applicable distribution period tables in the proposed regulations reflect longer life expectancies than the tables in the existing regulations.

Internal Revenue Service IRS Treasury. In general Tables V through VIII must be used if you made contributions to the retirement plan after June 30 1986. 1 substituted provisions relating to the application of this subsection to amounts received under annuity endowment or life insurance contracts which are not received as annuities and to amounts received as dividends for provisions which stated a general rule relating to the includability as gross income of amounts that were received under annuity endowment or life insurance contracts which were not received as annuities.

AnswerThe divisor is the number of years a person has left. For all subsequent years you must take the money out of your accounts by Dec. These tables correspond to the old Tables I through IV.

A tax-sheltered annuity plan often referred to as a 403b plan or a tax-deferred annuity plan is a retirement plan for employees of public schools and certain tax-exempt organizations. Actuarial tables under IRC Section 7520 provide the required standard factor for determining the value of a remainder interest in a CRUT. Using the life expectancy methodto determine the annual withdrawal for 1999 for a 40 year old.

How Many Years Can You File Back Taxes Annuity Filing Taxes Death Tax

Irs 2020 Tax Tables Deductions Exemptions Purposeful Finance

Life Expectancy Tables Actuarial Life Tables

Irs Usa

How To Avoid Paying Taxes On Social Security Income Paying Taxes Social Security Tax

1098 E User Interface Student Loan Interest Statement Data Is Entered Onto Windows That Resemble The Actual Forms Impo Irs Irs Forms Student Loan Interest

/ScreenShot2020-02-03at1.41.37PM-322605a2b23a49598d9cdf9faee0a97a.png)

Form 706 United States Estate And Generation Skipping Transfer Tax Return Definition

Account Ability Form 1098 User Interface Mortgage Interest Statement Data Is Entered Onto Windows That Resemble The Actual Accounting Irs Forms Spreadsheet

Ay0blaxtvo8c5m

Irs Issues Applicable Federal Rates Afr For April 2021

Approaching Age 72 Here S What You Need To Know About Rmds Fcmm Benefits Retirement

Https Www Irs Gov Pub Irs Pdf P6961 Pdf