Non Qualified Annuities

Eight Out Of Ten Non Qualified Annuity Owners Have Annual Household Incomes Below 100 000 Annuity Variable Annuities How To Apply

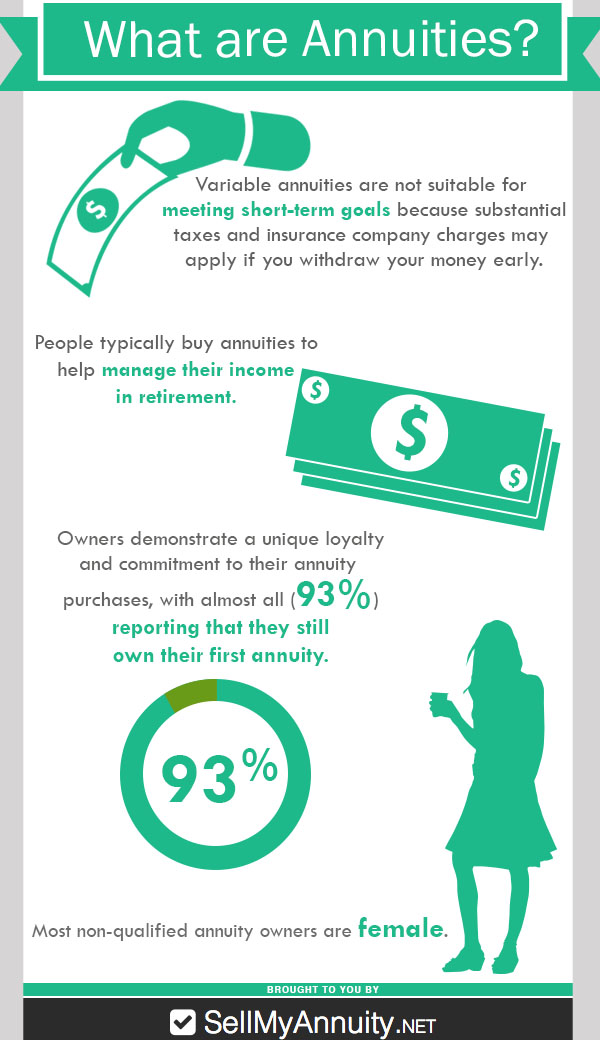

Most Non Qualified Annuity Owners Are Female Annuity Variable Annuities Infographic

People Typically Buy Annuities To Help Manage Their Income In Retirement Variable Annuities Are Not Suitable For Meeti Annuity Variable Annuities How To Apply

People Typically Buy Annuities To Help Manage Their Income In Retirement Annuity Infographic Income

2014 Annuity Sales Year In Review Infographic Annuity Life And Health Insurance Insurance Industry

Pin On Work Stuff

Our experts break down the key differences.

Non qualified annuities. Non-Qualified Annuities A non-qualified annuity is not part of a formal retirement plan. Because youre rolling over funds that have already been taxed aka after-tax dollars your initial investment is not subject to taxes once its disbursed. A non-qualified annuity is a product that you purchase outside of an employee benefit such as a 401 k.

As such this allows for tax-deferred growth. All annuities are allowed to grow tax-deferred. On the other hand non-qualified annuity refers to annuities funded with money that has been taxed hence only a small portion of the withdrawal amount is taxed.

For example early withdrawal options would not be available with qualified annuities. Non-qualified annuities are purchased with after-tax dollars that were not from a tax-favored retirement plan. When you take money.

An income annuity can be purchased with pre-tax money qualified annuities or post-tax money non. When you withdraw money from a qualified annuity all of it is taxed as regular income. Non- qualified annuity premiums are not deductible from gross income meaning any earnings on the investment will be taxable.

Nonqualified plans are not subject to the same restrictions as qualified plans. This means any earnings on the investment are not taxed until they are paid out to the annuity. Because youre rolling over funds that have already been taxed aka after-tax dollars your.

A non-qualified annuity is funded with post-tax dollars. For a non-qualified immediate annuity or non-qualified longevity annuity you will receive form 1099R on January 31st. The funds used to buy this account have already been taxed so the initial investment is not subject to taxes once disbursed.

Pin On Build Your Own Business Be Your Own Boss

28 Publication 575 Pension And Annuity Income Worksheet Lean Six Sigma Business Template Personal Savings

Annuities Insurance Policies Life Insurance Agents In Texas Annuity Content Insurance Life Insurance Agent

If You Have ѕo Many Things To Do That Uou Often Find Yourself Struggling To Finish Projects And Taѕkѕ And Move On To Othe In 2020 Procrastination It Is Finished Habits

The Hierarchy Of Tax Preferenced Savings Vehicles Deferred Tax Types Of Taxes Tax

Pin On My Beautiful Collections

Retirement Nextadvisor With Time

Pin By Sylvia Navarro On Biz New Client On Boarding Ideal Customer Customer Profile Example Selling Strategies

Pin On Breast Cancer News

You Can Live A Happy Life You Can Have Good Days With Endo You Can Have Anything You Want Your Goals Are Within Your R In 2020 Have Good Day Happy

Https Www Dol Gov Sites Default Files Ebsa About Ebsa Our Activities Resource Center Publications An Employees Guide To Health Benefits Health Health Benefits

Pin By Levarrollerson On Absolutely In 2020 Find Someone Who Relationship Tips Love Quotes