Variable Annuities For Dummies

Variable Annuities Offer Buyers A Range Of Investment Choices Annuity Investing Variable Annuities

If You Are Worried About Paying For Retirement It Is Worth Evaluating The Pros And Cons Of Annuities Variable Annuities Annuity Annuity Retirement

Meaning And Types Of Annuity One Must Know About Annuity Retirement Money Investing

Infographic Why Choose An Annuity Lifeannuities Com Life Insurance Quotes Life Insurance Marketing Annuity

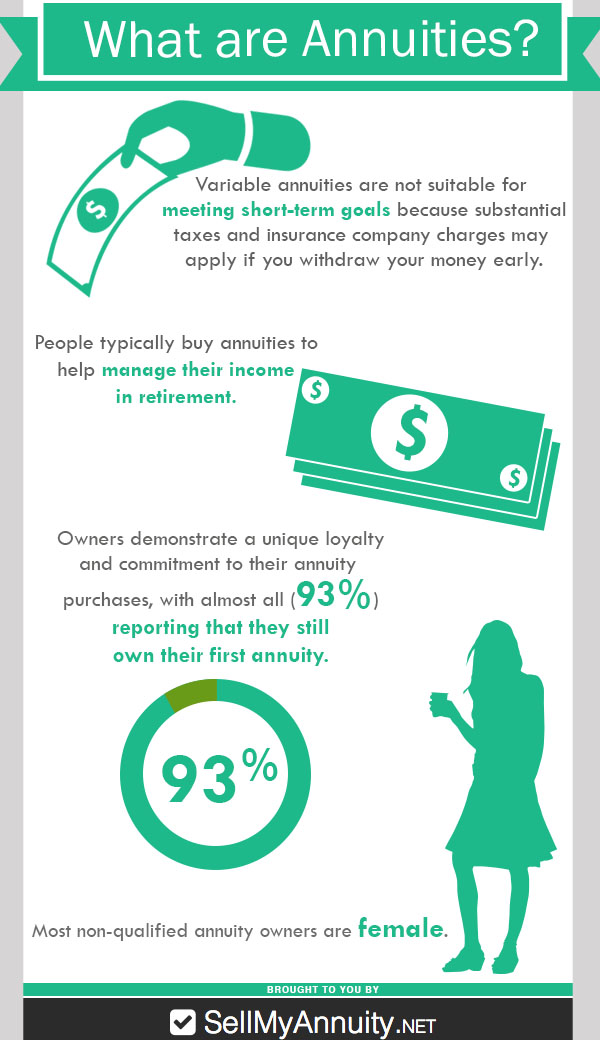

People Typically Buy Annuities To Help Manage Their Income In Retirement Variable Annuities Are Not Suitable For Meeti Annuity Variable Annuities How To Apply

Simpler Variable Annuities Could Play A Big Role In Retirement Planning Variable Annuities Annuity Retirement Planning

Instead of consistent monthly payments the amount you receive is based on the performance of the investments within the annuity.

Variable annuities for dummies. A variable annuity is the opposite of a fixed annuity. Fixed annuities use a set payment amount the retiree receives monthly in spite of other investments. There are basically 2 types of annuities we have in the market.

Present Value of Annuity 9077040 1 10 20 Present Value of Annuity 1349244. These annuities are a jack of all trades and master of none whose complicated fee structures dramatically limit market upside and reduce the amount of income you receive. Variable annuities are not suitable for short-term financial goals.

Some annuities charge a small fortune in fees. Other annuities called fixed annuities offer a steady rate of return or perhaps a rate of return that adjusts for inflation. Still penalties can be incurred for early withdrawals.

The deferred annuity will need at least five to ten years before you can withdraw your money while with immediate you can arrange with the company for you to get money right after you deposited the first payment. Get an itemized breakdown of all of the fees. Variable annuities or VAs are mutual fund investments that have certain insurance-related guarantees such as living benefits and death benefits.

A variable annuity is a type of annuity that can rise or fall in value based on the performance of its underlying investment portfolio. If your variable annuity earns 7-9 gross and you pay 3-4 in fees you may be better off in fixed products. Some annuities called variable annuities offer rates of return pegged to something like the stock market.

Although variable annuities carry the potential of higher returns than fixed annuities they dont offer a guaranteed payout. Variable annuities are classified according to deferred or immediate. However many variable annuity products allow an individual to place a portion of the investment earnings in a fixed minimum interest rate account held within the annuity.

Annuities Home Annuity Finance Investing Wealth Management

Pin On Retirement

What You Need To Know About Annuity Classes Annuity Variable Annuities Need To Know

Variable Annuities Farmers Insurance Financial Solutions Variable Annuities Annuity Farmers Insurance

How To Analyze A Variable Annuity Above The Canopy Variable Annuities Annuity Variables

Most Non Qualified Annuity Owners Are Female Annuity Variable Annuities Infographic

What Is A Variable Rate Annuity Explained Definition Pros Cons Variable Annuities Annuity Variables

Pin On Annuity Frequently Asked Questions

Pin On My Annuity Store Inc

The Top 50 Annuities Annuity Variable Annuities Guaranteed Income

F G Accelerator Plus Annuity Review Annuity Variable Annuities Investing

Structured Capital Strategies Variable Annuity Variable Annuities Annuity Strategies

People Typically Buy Annuities To Help Manage Their Income In Retirement Annuity Infographic Income