Variable Annuities Vs Mutual Funds

Annuities Vs Mutual Funds 11 Helpful Pros Cons 2021

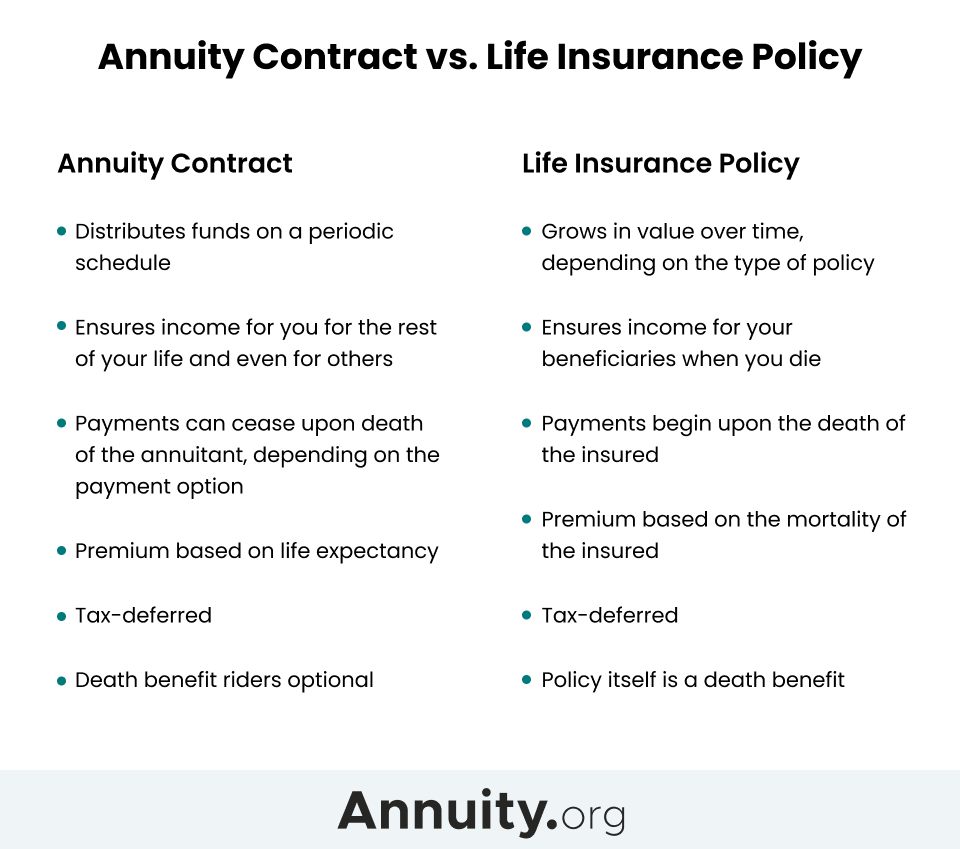

Annuity Vs Life Insurance Similar Contracts Different Goals

Variable Annuities Suck Archives Bankers Anonymous

Variable Annuities How Do They Work

What Is A Variable Annuity Due

Mutual Funds Vs Group Variable Annuities Planning For Retirement Fiduciaryfactor Com

In comparing variable annuities with mutual funds it is first important to understand the definitions and basic structure of both these types of investments.

Variable annuities vs mutual funds. Compare variable annuities and mutual funds from the viewpoint of both the issuing company and the contractholder with respect to a Taxes. Fees and the taxes also play a role. The percentage includes portfolio management administration distribution and other expenses.

Investments are made in mutual funds or mutual-fund-type accounts offered by the particular annuity. The investments are not tax-deductible since usually variable annuities are sold outside tax-deferred accounts as they already have a tax-deferred component. Regardless of whether your annuity is qualified or non-qualified the insurance company will be the account custodian.

C Mortality and expense risks. Thus comparing the tax consequences between a mutual fund and a variable annuity is difficult. Its a pooling of money to achieve diversification.

One significant difference between mutual funds and variable annuities is the account custodian. Mutual Fund Fees and Expenses. Variable annuities typically have more of them because of the insurance features.

The expense ratio is the funds ongoing cost of doing business. A variable annuity is a. Mutual funds may be purchased from the fund company directly or through a.

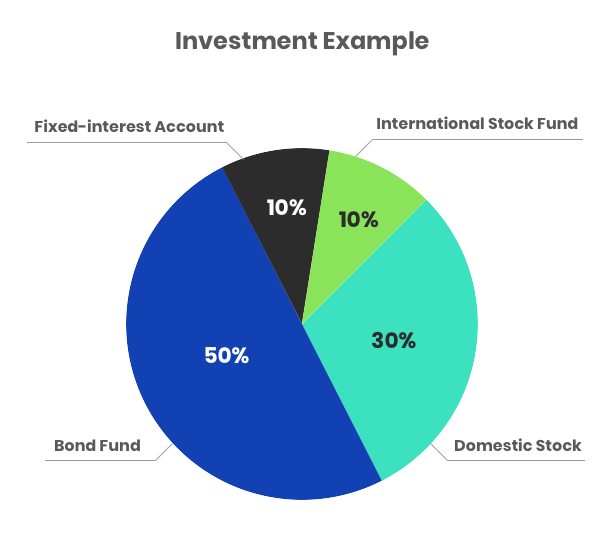

Mutual funds consist of a collection of different investments sold in shares and purchased by large numbers of individuals. Variable Annuities vs. CREF Equity Index Account Investment Product Commentary Account Performance Highlights In the first quarter of 2021 the CREF Equity Index Account produced positive returns that were slightly below those of its benchmark the Russell 3000 Index.

Fixed Annuities Introduction To Fixed Annuities

Recent Variable Annuity Innovations Provide Growth Safety Annuity Fyi

Variable Annuities Winning By Not Surrendering Insurancenewsnet

Variable Annuity Funds Vs Mutual Funds Trusted Choice

Variable Annuities What Are Variable Annuities Lifeannuities Com

Variable Annuity Definition Examples How Does It Work

Annuity Fund What Is An Annuity Fund How Does It Work

Annuities Vs Mutual Funds 11 Helpful Pros Cons 2021

Variable Annuities Planmember Retirement Solutions

Mutual Funds Vs Group Variable Annuities Planning For Retirement Fiduciaryfactor Com

Indexed Annuity Pros Cons Fixed Index Equity Index

Mutual Funds Vs Group Variable Annuities Planning For Retirement Fiduciaryfactor Com

Mutual Funds Vs Group Variable Annuities Planning For Retirement Fiduciaryfactor Com