Variable Annuity Vs Mutual Fund

Annuities Vs Mutual Funds 11 Helpful Pros Cons 2021

Variable Annuities Vs Etf Portfolios Seeking Alpha

Chapter 11 12

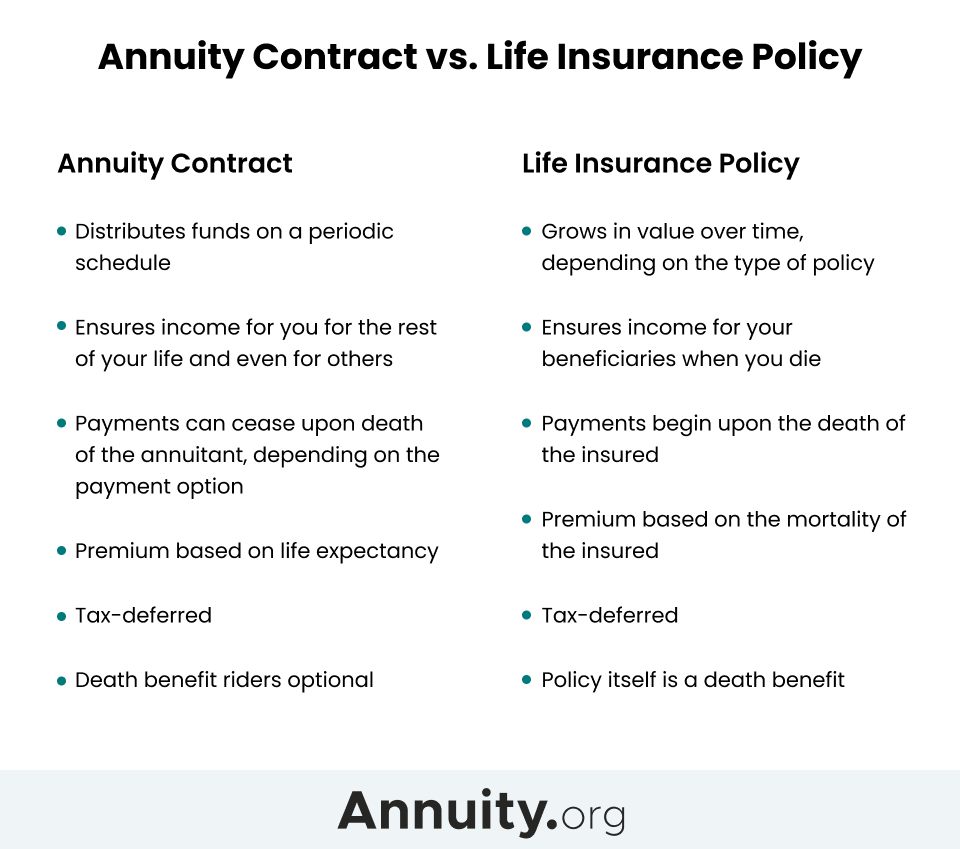

Annuity Vs Life Insurance Similar Contracts Different Goals

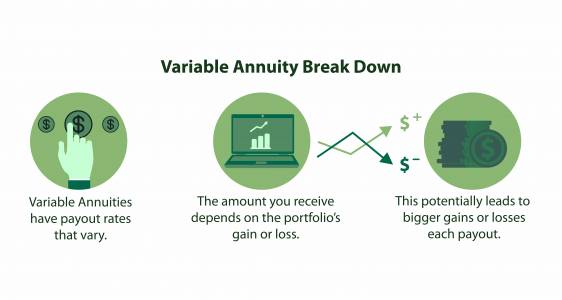

Variable Annuities How Do They Work

What Is A Variable Annuity Due

Mutual funds may be purchased from the fund company directly or through a.

Variable annuity vs mutual fund. Regardless of whether your annuity is qualified or non-qualified the insurance company will be the account custodian. Its also important to note that annuities are not investment securities. Variable annuities typically have more of them because of the insurance features.

Mutual funds consist of a collection of different investments sold in shares and purchased by large numbers of individuals. Variable annuity mutual funds and mutual funds are cousins not identical twins. While the fees of an annuity may be 1 higher than those of mutual funds it seems that this would be offset by the tax deferral advantages.

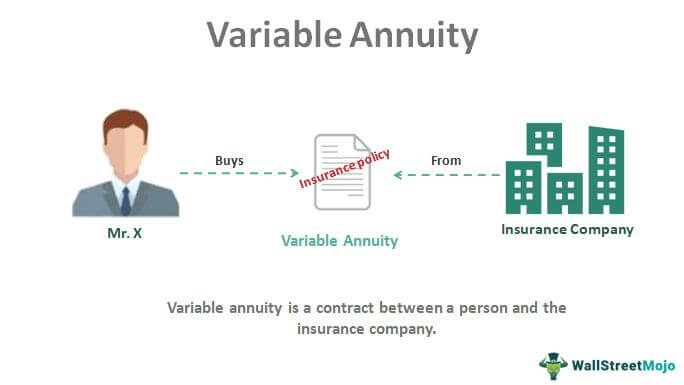

A variable annuity is basically a mutual fund inside a tax-deferred insurance wrapper. Variable annuities are purchased directly from life insurance companies. Those payments can be set up for the rest of your life or for the life of your spouse using something called an income rider.

The investments are not tax-deductible since usually variable annuities are sold outside tax-deferred accounts as they already have a tax-deferred component. One significant difference between mutual funds and variable annuities is the account custodian. In fact variable annuities offer a menu of investments that look just like mutual funds called subaccount funds.

They are insurance products. If the company is not in Phase II there would be no tax at all. There are equal number of pros and cons of variable annuities if you compare them with mutual funds.

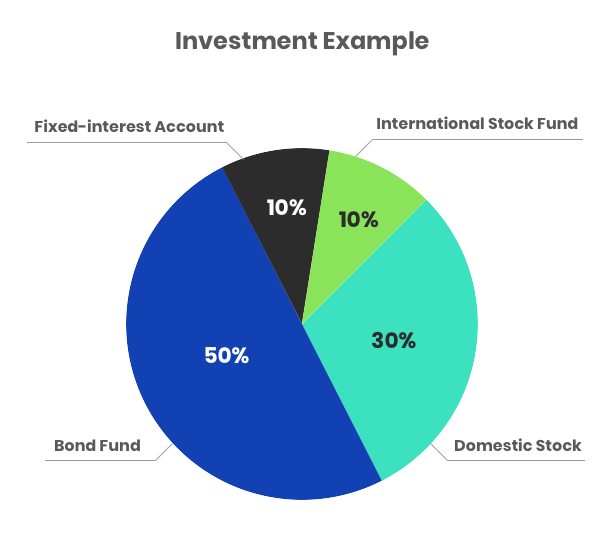

Its a pooling of money to achieve diversification. Investments are made in mutual funds or mutual-fund-type accounts offered by the particular annuity. If it is in Phase II the tax would be at essentially a rate of 25 per cent.

Variable Annuity Funds Vs Mutual Funds Trusted Choice

Variable Annuities Suck Archives Bankers Anonymous

Variable Annuities Winning By Not Surrendering Insurancenewsnet

Recent Variable Annuity Innovations Provide Growth Safety Annuity Fyi

Variable Annuity Definition Examples How Does It Work

Mutual Funds Vs Group Variable Annuities Planning For Retirement Fiduciaryfactor Com

Variable Annuities What Are Variable Annuities Lifeannuities Com

Annuities Vs Mutual Funds 11 Helpful Pros Cons 2021

What Is A Variable Annuity How Does It Work

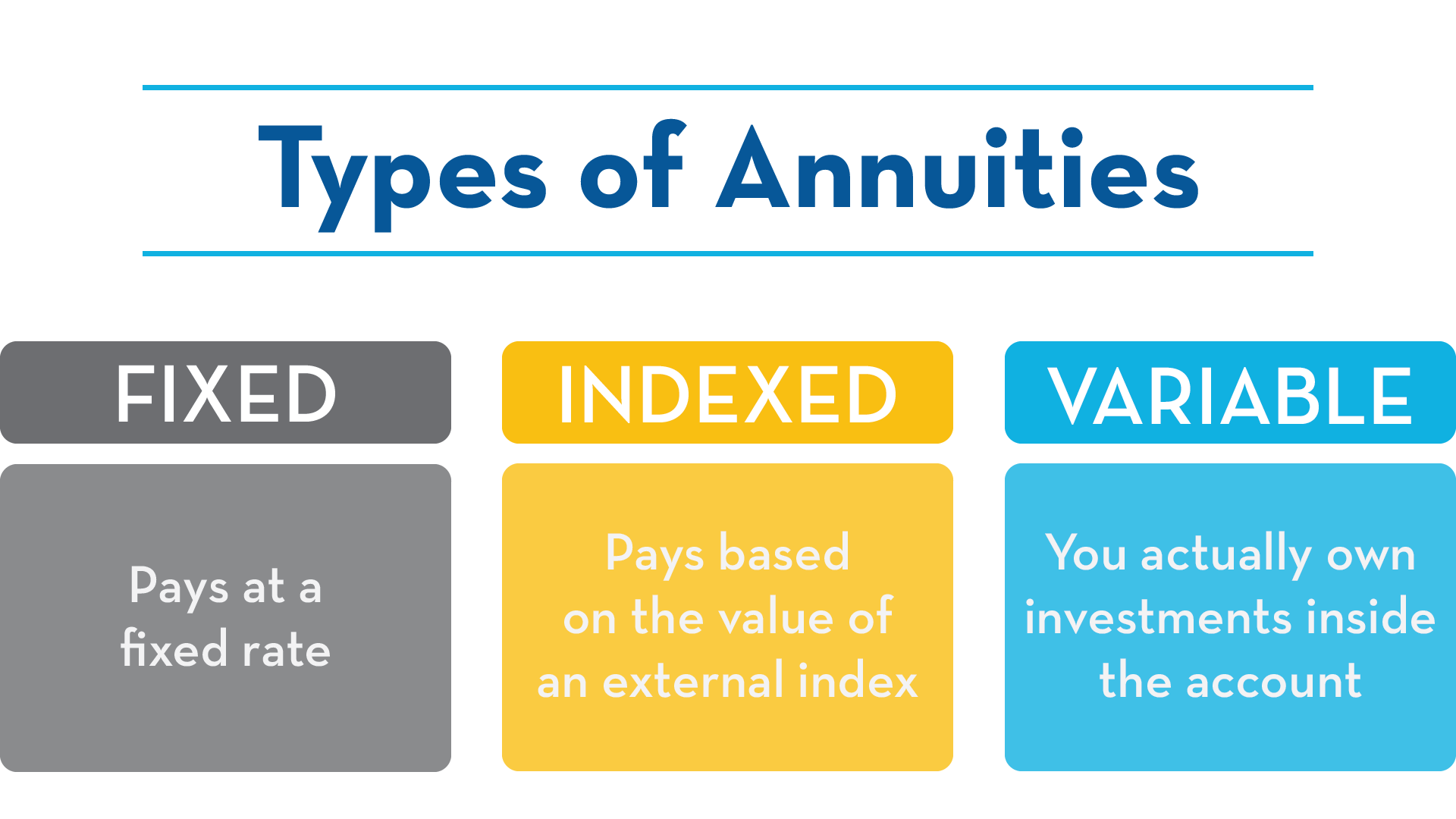

Fixed Annuities Introduction To Fixed Annuities

Which Is Better The Mutual Fund Or The Variable Annuity

What Is A Variable Annuity Due

Mutual Funds Vs Group Variable Annuities Planning For Retirement Fiduciaryfactor Com