Indexed Annuities Problems

Indexed Annuity Pros Cons Fixed Index Equity Index

Pin On Nerd S Eye View

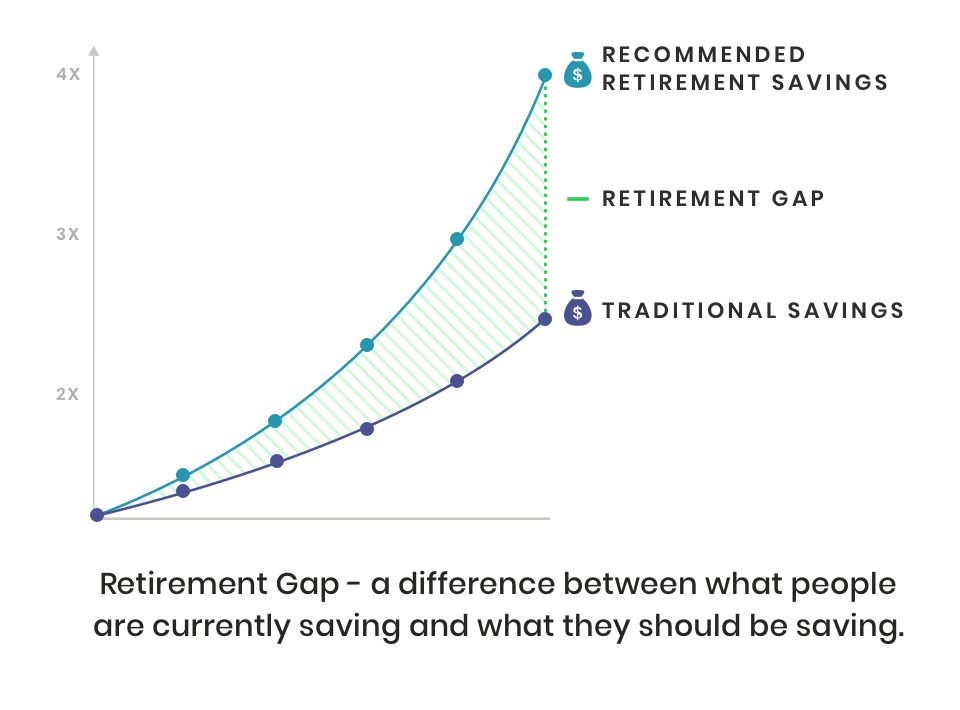

Financial Freedom Pyramid

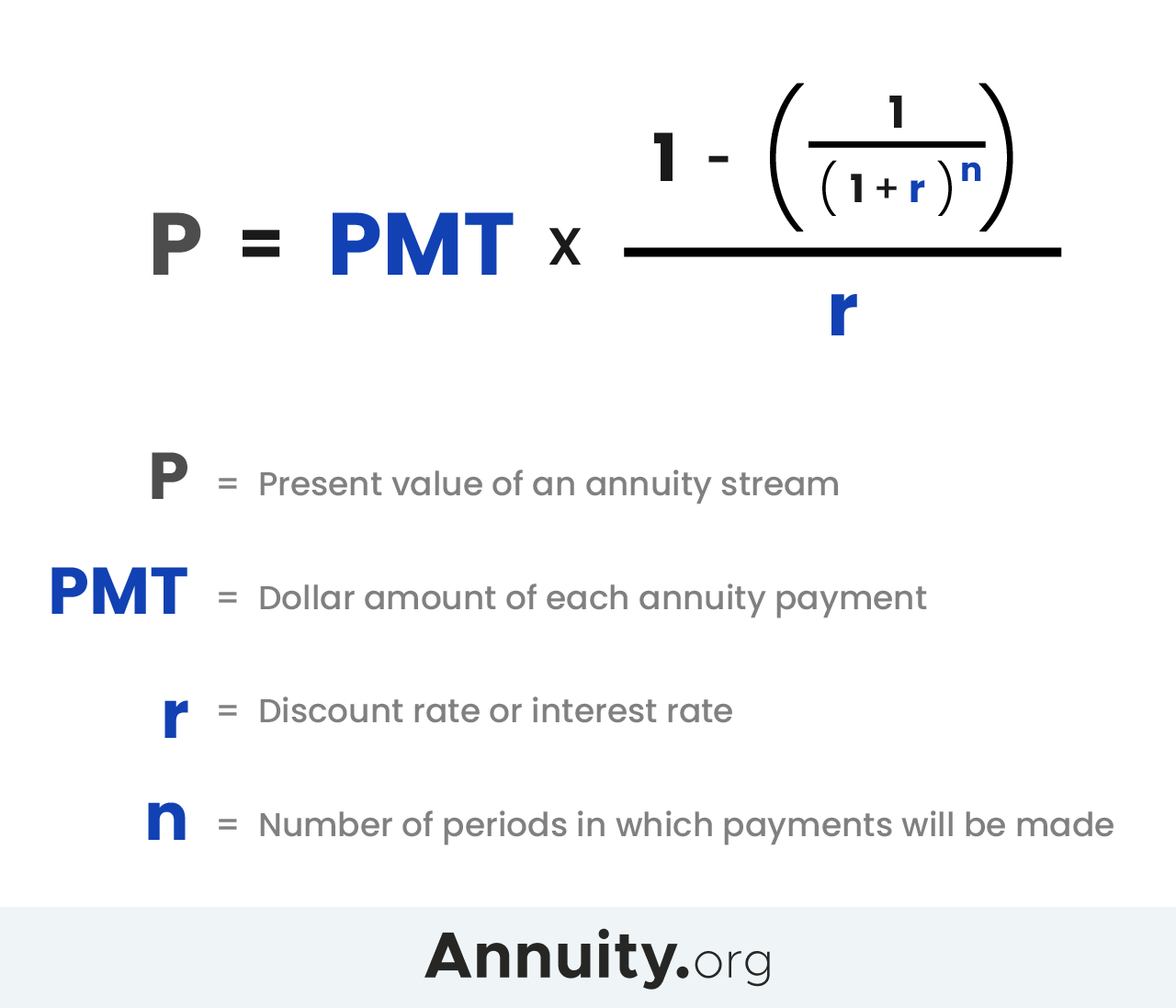

:max_bytes(150000):strip_icc()/CalculatingPresentandFutureValueofAnnuities1-0cea56f3b4514e44bed8f45d9c74011e.png)

Calculating Present And Future Value Of Annuities

Hsc Syjc Commerce Insurance And Annuity Chapter 3 Maths 2 Annuity Math Math 2

:max_bytes(150000):strip_icc()/CalculatingPresentandFutureValueofAnnuities5-d76f3a6c09a54703afa365a16aff6607.png)

Calculating Present And Future Value Of Annuities

Fixed index annuities offer some of the upside of.

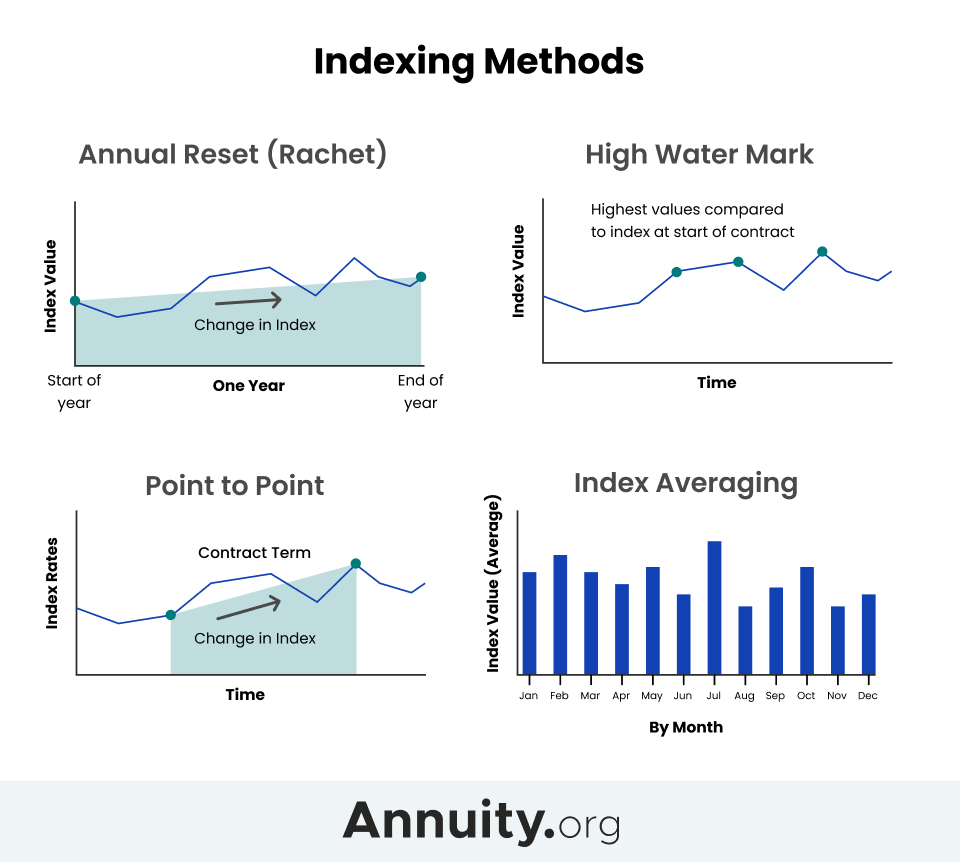

Indexed annuities problems. Participation Rate and Low Cap Limit Returns. The disadvantages of annuities depend on the type of annuity. One of the failures of financial regulations including.

In the simplest terms when you first purchase an equity indexed annuity the value of a chosen index typically the SP 500 is notated and becomes the benchmark for future gains. More problems with indexed annuities There are other issues to consider too. In return for that safety your potential gains are normally capped ie determined by a cap rate or participation rate.

Indexed annuity proponents may point to the risk management benefits of the product in trying to reconcile these statistics. The indexed annuity returned 189 per year. The result is a greater potential upside than a traditional fixed contract with less risk than a variable annuity.

There are actually no FIA providers with an A rating. Following are some of the problems with this annuity type. A fixed index annuity provides steady payments that are based on the performance of an underlying index.

There are a few problems. They do not directly participate in any stock or. Fixed indexed annuities are insurance products that are designed to help you manage certain financial risks associated with retirement such as volatile markets falling interest rates and longevity.

So if a client was sold a 200000 annuity the salesperson might take home 14000 up front. On your contract anniversary date if the value of the index again in this case the SP 500 is higher than it was when you first opened the annuity your account will be credited with the relevant percentage increase. This latter problem is severe considering Americans are living longer lives in retirement.

Pin By Phillip Wasserman On The Anti Annuity Universal Life Insurance Annuity Single Premium

Annuity Contract For Cash Inflows Outflows Example Calculations Annuity Finance Quotes Finance Class

:max_bytes(150000):strip_icc()/CalculatingPresentandFutureValueofAnnuities3-f5e4d156c37b4fffb4f150266cea32b1.png)

Calculating Present And Future Value Of Annuities

Annuity How Annuities Work Rates Types Pros Cons

Index Universal Life Vs 401k Which Is Better For Retirement Retirement Planning Saving For Retirement Universal Life Insurance

Financial Planning Report Myfinancialplannerin Financial Planning Financial Planner Financial

Earn Up To A 15 Bonus For Signing Up On This Popular Retirement Savings Plan Low Fees Safe Gr Annuity Retirement Savings Plan Safe Investments

Present Value Of An Annuity How To Calculate Examples

Pin On Cool Memes

New Annuities Starting To Address Rmds Investmentnews Wealth Transfer Annuity Tsunami

Pin On Job Shirts

Central Provident Fund Cpf Scored A B For Global Pension Index Why Did We Not Score An A Life Annuity How To Plan Retirement Accounts

Preparation Ecn Residanat Mesothelioma Law Firm Donate Car To Charity California Donate Car For Tax Credit Car Insurance Car Insurance Uk Low Car Insurance